Everything you need to know about payday loan criteria but were afraid to ask...

If you’d like to know more about eligibility criteria for payday loans, but don’t know where to start, you’ve come to the right place. We’ve put together a guide to help consumers navigate the choppy waters of the payday loans market.

Ever wondered what the absolute basic criteria are that all payday loans lenders will ask for? Or whether you can apply for a payday loan with a poor credit rating, or without a bank account? Read on.

What’s the difference between a payday loan and a normal personal loan?

Unsecured personal loans usually work like this:

- You agree a loan amount and a repayment term with your lender

- You repay a certain amount, plus interest, over a set period of time, in monthly instalments

- You must repay the entire loan amount over the pre-agreed term

Unsecured payday loans usually work like this:

- You agree a loan amount with your lenders

- You pay back the full amount, plus interest, in a single instalment once you have been paid

In short, payday loans are different from regular personal loans because they are small, short-term loans that charge very high interest. They are repaid as soon as you have the money in your bank to do so.

What’s the difference between payday loans and instalment loans?

Instalment loans are a more flexible version of payday loans. When you take out an instalment loan, you agree to the loan value and the repayment term at the beginning of the loan. This will still be a very short-term period, usually up to a few months. You then repay the loan in several monthly instalments until it is cleared.

You still usually pay higher interest for an Instalment loan, but some borrowers prefer to spread the cost of repayment over several months. This can help to prevent borrowers getting into a similar financial fix time and time again.

Get your facts right

There’s no denying that payday loans and other short-term loans are generally more expensive than normal longer-term personal loans and there are a number of reasons for this.

Payday loans are expensive because….

- The default rate is higher, so it’s riskier for lenders

- The costs involved with lending over a short period are similar to the cost involved with lending over a longer period

- Borrowers receive fast decisions and get quick funding, which also costs the lender money

So maybe payday loans aren’t as expensive as they seem?

Interest rates will usually be higher than longer-term loans, but you will repay faster. Also - using the Annual percentage rate (APR) to measure or compare the cost of payday loans is pretty much useless. This figure shows the cost of the loan as a percentage of the loan value, over a year. Payday loans are taken out over a month or so and are very small in value, hence the APR is enormous and unrepresentative of the actual cost of borrowing.

What are the minimum payday loan lending criteria?

Most payday lenders will consider applications from a wide range of prospective borrowers, including those who might not have the most perfect credit background. This is great, from a consumer perspective, but there are a few minimum payday loan requirements that almost all lenders will want you to meet before they’ll even look at your application:

- You are over 18 years old

- You have a UK bank account

- You are a UK citizen

Responsible lenders, registered and authorised by the Financial Conduct Authority (FCA) should go a little further in applying minimum lending criteria. Responsible direct lenders may also look for the following minimum lending criteria for payday loans:

- A regular income

- Employment (full-time or part-time)

- A minimum income amount

- No history of CCJs or bankruptcy

If you meet these three basic payday loan criteria, you can usually apply for a payday loan. However, to have a realistic chance of being approved for a payday loan, you will have to meet certain other eligibility criteria for payday loans. We’ll look at these in a little more depth:

Your credit history

Payday lenders registered by the FCA will have to carry out a creditworthiness assessment before entering into a credit agreement with you, This can take several forms, depending on what the lender deems necessary and relevant. But it should be sufficient to make sure the lender is confident that you will be able to make the repayments as agreed.

The same goes for lenders assessing an application for an increase in loan amount or a further loan on top, or following, an existing loan.

If you have had problems repaying loans in the past, you may still be accepted for a payday loan and you are free to apply, providing you meet the other minimum requirements. However, your credit rating may have an impact on the amount of loan you will be offered and the interest rates you will pay, so you will usually get a better deal if you have a better credit record.

What if I’m bankrupt or have CCJs?

There are certain credit problems that will be viewed more negatively than others. These include County Court Judgments (CCJs), which have yet to be settled, and bankruptcy. If you have either of these on your record, you may struggle to secure a payday loan with a responsible lender, and considering a lender not registered with the FCA is not recommended and could lead to more serious financial problems.

Your income

Having a regular income is one of the main things a payday lender will look for when deciding whether they should approve your application. After all, if you don’t have a regular income, you won’t be able to predictably repay a loan.

Some direct lenders will insist that you have a minimum income, such as £1,000 per month, for example. This helps them to avoid lending to people who have very low income and who are unlikely to be able to repay a loan without leaving themselves financially vulnerable by doing so.

Employment

Most FCA-registered short term or payday lenders will check that you are employed before agreeing to lend you money. Although an employment contract can end, leaving a borrower in a difficult financial position, being employed at the point at which your credit agreement is signed, is usually a minimum lending criteria.

Some responsible lenders might accept self-employed applicants, especially if they can demonstrate a solid regular income. However, most lenders still view self-employment as a less predictable source of income.

What are the alternatives for people who don’t meet the payday loan lending criteria?

If you are looking for a personal loan of some kind, but are either unemployed, lack a large enough regular income, or have a poor credit history, there are alternatives to consider.

Guarantor loans

These are personal loans that are taken out by a borrower, but guaranteed by a loved one who agrees to cover the debt if the borrower is not able to. Lenders check both the borrower’s and the guarantor’s credit history and financial details before agreeing to a guarantor loan and both parties stand to incur damage to their credit file if the debt is not repaid on time.

Overdrafts

You may find that your bank account provider may consider opening an overdraft facility on your account if you need a small amount of cash to tide you over. Overdrafts do charge interest, but you can minimise these costs by paying them off in full each month.

Borrowing from friends or family

This may seem like an option that you would rather avoid. But many people are surprised how willing loved ones are to help you out over a short period. Everyone struggles from time to time and there’s no shame in asking for help.

Agreeing a payment plan

If you were looking to borrow money to repay another debt, perhaps the best solution is to approach the company you owe money to and ask them for a new payment plan. Being honest is always the right policy when it comes to debt. Most responsible lenders will help you repay in a way that you can afford, over a longer period, or with a payment break, for example.

Signing up to a credit union

Credit unions are an old fashioned concept that still have a place in helping people access credit when they need it, regardless of their situation. The idea is that you become part of a community that pays into the credit union, which then lends out to members when they need it.

Finally, always remember to consider the above alternatives before applying for a payday loan. If you can get by without applying for emergency loans or other short-term loans, then you should try to avoid getting into debt. Make any changes you can to minimise your expenditure and communicate with your creditors to try to work out payment plans.

If you do decide to go ahead with applying for a payday loan, only consider those who are registered with the FCA and who lend responsibly.

Moneyboat's service is rated Excellent

Blog Disclaimer

We do all we can to bring you interesting, practical and valuable information. However, please understand the following:

- Moneyboat.co.uk are in no way connected or affiliated with the application or affiliate links mentioned in this or any article. We do not receive any commission and are not responsible for any charges that may result from any free trials or paid subscriptions.

- Moneyboat.co.uk does not provide medical advice It is intended for informational purposes only. It is not a substitute for professional medical advice, diagnosis or treatment. Never ignore professional medical advice in seeking treatment because of something you have read on the site. If you think you may have a medical emergency, seek medical advice immediately or dial 999.

- Information and data on this blog are for information purposes only. While we work hard to ensure it is accurate, we cannot accept responsibility for the accuracy, completeness, suitability or validity of any information provided on the blog. We will not be liable for any errors, omissions, losses, injuries or damages arising from its display or use. All information is provided with no warranties and confers no rights.

If you feel that any of the information published on our blog is not accurate, please notify us via email at thecrew@moneyboat.co.uk.

Representative Example: Borrow £400 for 4 months, 4 monthly repayments of £149.37. Total repayment £597.48, interest rate p.a. (fixed) 255.5%. Representative APR 939.5%.Compare Moneyboat loans.

Warning: Late repayments can cause you serious money problems. For help, go to www.moneyhelper.org.uk.

Latest blog posts

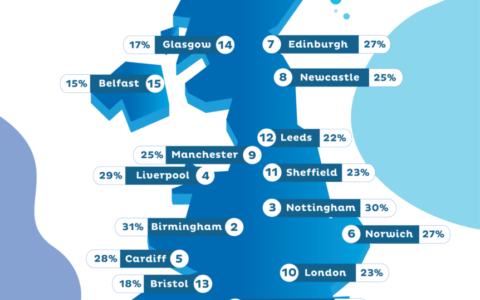

UK Credit Score Index

Curious about UK credit scores and public perceptions? We dive into the world of credit scores and uncover the real emotions and myths around them.