The Emotional Spending Crisis: Are Brits trying to buy their way out of stress?

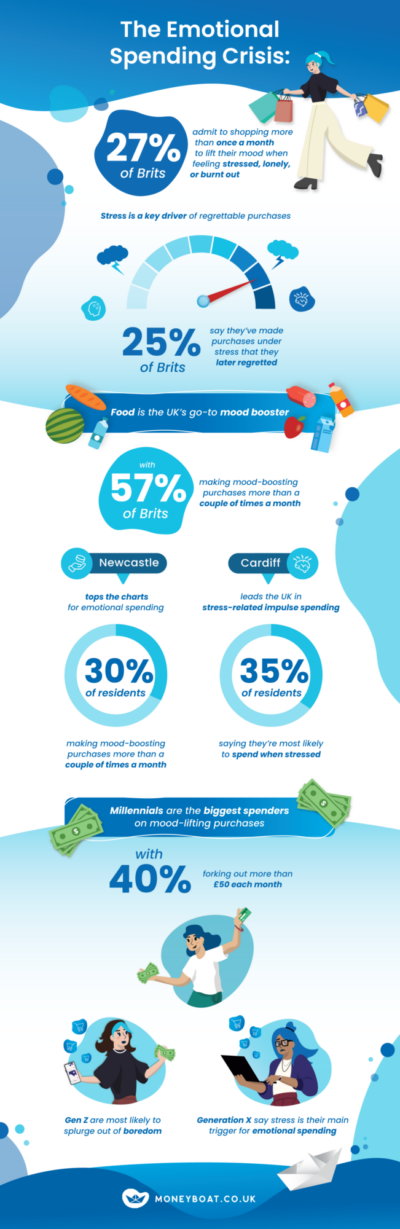

Over a quarter of Brits (27%) admit to shopping more than once a month to lift their mood when feeling stressed, lonely, or burnt out. Whether it’s a pair of shoes on sale, new gadgets, a daily sweet treat, or impulsively signing up to a gym membership, it’s easy for our wallets to become led by our emotions.

People are increasingly turning to purchases as a way to cope with the pressures of modern life. Meanwhile, others take comfort in spending even if it’s beyond their means.

But what are the common triggers for emotional spending? And does it vary by age and location? We surveyed 1,000 adults in the UK to uncover why we turn to spending as a pick-me-up, exploring which regions are most likely to express their emotions at the checkout.

In this guide:

- Top emotional spending triggers in the UK

- Emotional spending patterns by region

- Which generations use spending to feel better?

- Tips for how to stop emotional spending

Top emotional spending triggers in the UK

Diving into emotional spending psychology, we found that boredom is the biggest emotional trigger for impulse spending in the UK. What’s more, one in three (30%) Brits admit that simply feeling bored can push them to spend money they don’t have.

Stress is the next big influencer, affecting more than 25% of Brits. Meanwhile, more than a third (34%) of those surveyed admit that they’ve made purchases under stress that they later regretted.

When it comes to comfort spending, food is the UK’s go-to mood booster, with almost three in five people (57%) saying it’s their most common emotional purchase. Closely followed by clothes and fashion, material objects are some of the easiest items to add to basket when we’re feeling low, or looking for a quick pick-me-up.

Though many of us look to the shops to help fix our mood, almost a quarter of Brits (24%) admit that spending has had the opposite effect – negatively impacting their wellbeing.

Emotional spending patterns by region

More than one in five people (22%) reach for their wallet to lift their spirits at least a few times a year, showing that emotional spending is a challenge many of us face. But how do shopping habits vary across the country? We analysed how adults across the UK spend money to cheer themselves up.

Newcastle tops the charts for emotional spending, with one in three (30%) residents making mood-boosting purchases more than a couple of times a month. Meanwhile, Mancunians are the most generous with themselves. More than a third (34%) of those from Manchester spend over £50 a month on treats and feel-good buys.

Elsewhere, spending is used to soothe worry and restless thoughts. Cardiff leads the UK in stress-related impulse spending, with 35% admitting that they’re most likely to spend when they’re feeling stressed. Likewise, anxiety is the top emotional trigger for impulse shopping in Bristol, according to 33% of residents.

In Sheffield, nearly half (47%) say that boredom is the number one reason why they spend impulsively. Meanwhile, Glasgow ranks highest in alcohol-related emotional spending. Almost half (47%) of residents say they buy alcohol to lift their mood.

Which generations use spending to feel better?

How do different generations use spending to cope with stress and emotions? We found that age and life stage play a big role in our relationship with emotional spending.

Surprisingly, Generation X are the most frequent spenders, with 26% indulging more than twice a month to improve their mood. While Gen Z is most likely to splurge out of boredom, Gen X say stress is their main trigger for emotional spending.

Millennials are the biggest spenders on mood-lifting purchases, with 40% forking out more than £50 each month. They’re also the most likely to treat themselves several times a week, with one in 12 (8%) turning to impulse purchases for comfort when feeling stressed, lonely or burnt out.

Though they’re the most likely to spend money to alleviate stress, Millennials say that emotional spending has had a negative impact on their financial wellbeing—compared to 78% of Boomers who say it hasn’t affected them at all.

Tips for how to stop emotional spending

More than one in five Brits (22%) spend more than £50 a month on little ‘treats’ and purchases to help lift their spirits. That’s £600 a year.

Retail therapy isn’t always a bad thing. But if we do it too often, it can begin to impact our short-term budgets and long-term financial goals. So, if you’re feeling the pinch of impulsive spending, there are plenty of mindful actions you can try to help you reflect before you commit to checkout.

1. Redefine what you count as a treat

If you often find yourself buying non-essential items to soothe stress, reconsider what you define as a treat. Make a list of feel-good activities that don’t require spending and keep them to hand the next time you feel tempted to reward yourself with another purchase.

Whether it’s taking a walk, cuddling your pets, watching a good movie, doing some yoga or exploring somewhere you’ve never been before – there are plenty of ways to get a dash of dopamine without spending a penny.

Our guide to free and low-cost weekend activities explores how to make the most of deals and offers to help you save some cash.

2. Plan your monthly spending

Creating a consistent monthly spending budget can help you gain a sense of control and awareness over your spending habits. For instance, budgeting methods like the 50/30/20 rule can help you break down your earnings into essential costs, wants and savings contributions. That way, you can rest assured that your priority expenses are covered, and you’re gradually building your savings.

What’s left over is known as your discretionary income – the money you have left to spend on non-essentials. When it comes to spending, it’s often helpful to create a list of things you need or want to buy each month and order them by priority.

If you don’t get around to the last items on your list, consider them as you write your next month’s list and see if they’re still a priority.

See what’s possible and learn more about maximising your savings with our guide to how much you could save in a year.

3. Make it a challenge

Sometimes one of the most effective ways to motivate yourself to cut your spending is to make it a challenge. Budgeting challenges can be a fun and rewarding way to create positive habits and take a break from impulsive purchases.

Try budgeting techniques like the no-spend challenge, setting yourself the task of pausing spending on anything non-essential for a day, a week, or a month. How you commit to the challenge is up to you and your goals, so it’s an easy one to trial.

4. Embrace the one in, one out rule

Our survey found that fashion, tech and beauty items are the most common mood-boosters in the UK, after food. If you find yourself drawn to buying clothes, books, and homeware when you’re feeling happy, sad or stressed, consider the one in, one out rule.

The one in, one out rule is a common decluttering method where for every new item you buy, you remove a similar item you already own. Not only can this help simplify what you own, but it can also help to encourage more mindful purchases. Considering the value of each item can help you decide if it’s the right choice for you right now.

5. Ask yourself these questions before you purchase

Before making a purchase, it can be helpful to pause and consider the value of each item in more detail. We’ve gathered some helpful questions to consider before you reach for your wallet or add something to your basket:

- Do I need it?

- Do I need it right now?

- Will I use this more than 30 times?

- Do I have room for it?

- Will I actually use this?

- Is my money better spent elsewhere?

- Do I have something similar already at home?

Reflecting on the reasons why you want to spend can also help you recognise your emotional spending triggers. For instance, are you:

- Hungry

- Thirsty

- Bored

- Anxious

- Stressed

It’s easy for spending to feel urgent, especially if something is on sale. But taking a mindful approach to purchases can help you reassess if it’s worth your money right now.

Discover more helpful resources

Life is about balance. It’s okay to enjoy treats and reward yourself and your loved ones with special purchases! Managing emotional spending isn’t about removing purchases entirely – it’s about controlling your finances and recognising your impulses, so your spending doesn’t control you.

Understanding the signs of emotional spending and finding tools to make more intentional purchases can help you appreciate the little joys in life as well as stay on track with your goals.

For more helpful financial insights, head to our Moneyboat blog for guides on how to boost your savings, including how to create long-term financial goals.

If you’re ever feeling low or burnt out and need someone to talk to, you’re not alone. Help is always available. You can reach out to organisations such as Mind and Samaritans for free and confidential mental health support. For more guidance, visit our complete list of third-party support organisations and charities.

Methodology

Moneyboat conducted a national survey via TLF. The survey polled 1,000 UK adults between 28.07.2025 and 30.07.2025. The questions in the survey are displayed throughout the above content, and the data includes splits across age groups (18-24, 25-34, 35-44, 45-54, 55-64, 65+), Income (£9,999 or less, £10,000 to £15,000, £16,000 to £20,000, £21,000 to £25,000, £26,000 to £30,000, £36,000 to £40,000, £41,000 to £50,000, £51,000 to £60,000, £61,000 to £70,000, £71,000+).

Blog Disclaimer

We do all we can to bring you interesting, practical and valuable information. However, please understand the following:

- Moneyboat.co.uk are in no way connected or affiliated with the application or affiliate links mentioned in this or any article. We do not receive any commission and are not responsible for any charges that may result from any free trials or paid subscriptions.

- Moneyboat.co.uk does not provide medical advice It is intended for informational purposes only. It is not a substitute for professional medical advice, diagnosis or treatment. Never ignore professional medical advice in seeking treatment because of something you have read on the site. If you think you may have a medical emergency, seek medical advice immediately or dial 999.

- Information and data on this blog are for information purposes only. While we work hard to ensure it is accurate, we cannot accept responsibility for the accuracy, completeness, suitability or validity of any information provided on the blog. We will not be liable for any errors, omissions, losses, injuries or damages arising from its display or use. All information is provided with no warranties and confers no rights.

If you feel that any of the information published on our blog is not accurate, please notify us via email at thecrew@moneyboat.co.uk.

Representative Example: Borrow £400 for 4 months: 3 monthly repayments of £156.09 followed by a final repayment of £156.07. Total repayment £624.34. Interest rate p.a. (fixed) 288.35%. Representative 1,267.9% APR.

Compare Moneyboat loans.

Warning: Late repayments can cause you serious money problems. For help, go to www.moneyhelper.org.uk.

Latest blog posts

Short-term loans and their advantages

Explore the advantages and disadvantages of personal short-term loans, including payday loans, so you make the right decision when you need funds fast.

How to build an emergency fund

Ready to get started on building an emergency fund? Learn what an emergency fund is, how much to save, and how it can help you avoid short-term borrowing

How to borrow money from family and friends

Learn about family and friend loan agreements and the pros and cons of borrowing money from your loved ones – check to see if it's a good option for you!

What is the difference between APR and interest rate?

Learn the difference between APR and interest rate, how each affects borrowing costs, and why both matter when comparing loans.

Can you pay off a payday loan early?

Wondering if you can pay off a payday loan early? Learn how early repayment works, the pros and considerations, and what to check before you repay.

Why can’t I get a loan?

Wondering why you’ve been refused for a loan? We explore the most common reasons lenders say no, as well as how to increase your chances of approval.

What is a pre-approved loan?

Curious about pre-approved loans and how they work? Find out what loan pre-approval means, whether it guarantees acceptance, and if it’s right for you.

What is an authorised push payment scam?

Curious about authorised push payment scams and how you can protect yourself from fraudsters? Learn about the warning signs and the most common types of scams.