UK Credit Score Index

In today's fast-paced world, credit scores play a starring role in our financial dramas. They're the magic numbers that determine if we get that loan, secure a credit card, or even land a dream job or house. But let's be honest, credit scores can seem like a mystery to many people. So, how do folks in the UK really feel about their credit scores, and do they even keep track of it?

We conducted a survey across the cities and towns of the UK to reveal how Brits feel about their credit scores if they understand their credit scores, and what they think impacts them the most. Don't worry, we've got your back with practical tips on boosting your score too, and how to keep it healthy through all the ups and downs of life.

Our survey analysis

Understanding credit scores is a critical aspect of personal finance. Our analysis of credit score awareness among Brits sheds light on some key insights.

What is your credit score?

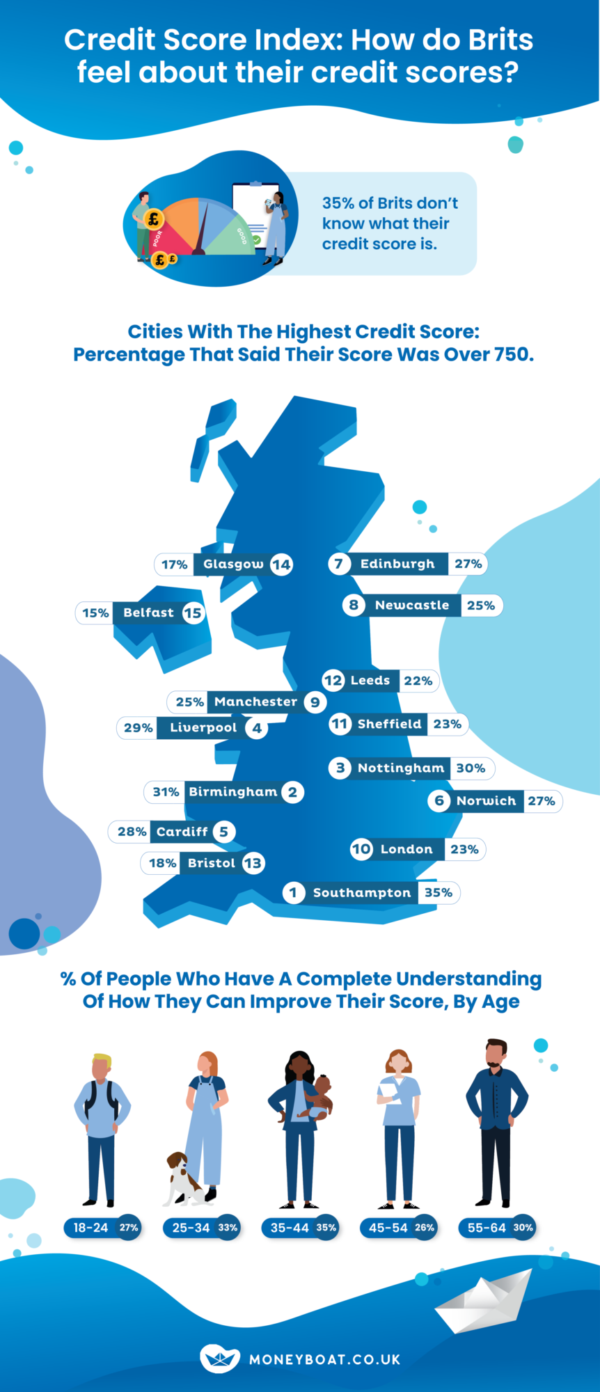

The first question we asked was: do you know what your credit score is?

Astonishingly, 35% of Brits are unsure about what their credit score is. This is a substantial gap in the population’s financial knowledge that needs to be addressed, as credit scores heavily influence your access to credit, mortgages, and job opportunities.

On the positive side, 40% of Brits have credit scores exceeding 500, indicating responsible financial management and better access to financial products. Cities where people said their credit score was over 500 included Glasgow and Nottingham, with over 50% of inhabitants claiming a perfect credit score. Meanwhile, Bristol and Belfast had the lowest number of people with 500 credit scores, less than 35% each.

Age significantly impacts credit score awareness. Young adults (18–24) are more informed, with only 15% unsure of their scores, while 45–54-year-olds show a higher 41% uncertainty. Our analysis also reveals a minor gender divide, with 37% of women and 33% of men being aware of their credit scores. This calls for inclusive financial education and awareness initiatives.

Do you understand how credit score bands work?

The data shows that about 18% of Brits don't understand how credit scores work but on the bright side, around 59% of people do have some level of understanding. Now, when we look at the difference between men and women, it's interesting. A larger group of men (29%) completely get how credit scores work, compared to women (19%).

So, more men have the full picture. This suggests that many people know something about credit scores, but men tend to understand them better than women.

Are you happy with your current credit score?

Most Brits, around 77%, are happy with their current credit scores. This happiness varies with age, as those over 65 (83%) and people aged 55 to 64 (81%) are the happiest, followed closely by 25 to 34-year-olds (80%). Additionally, slightly more women (78%) are content with their credit scores compared to men (77%).

In terms of location, folks in Belfast are the happiest, with a remarkable 89.7% expressing contentment, while people in Manchester are the least happy, with only 52.7% satisfied. These differences might be due to local economic conditions and financial habits.

Would you know how to improve your credit score?

The data tells us that when it comes to improving their credit score, 16% of Brits don't know where to start, while nearly 30% fully understand how to do it, and the rest have a partial grasp. 32% of men have a complete understanding, compared to 27% of women.

In terms of age, 35–44-year-olds are the most knowledgeable, with 35% having a complete understanding of how to boost their credit score, followed by those aged 25-35.

Which factors do you think impact your credit score?

Our survey respondents identified 12 different factors that they felt impacted their credit scores:

Missed credit payments - 69%

Multiple credit applications - 62%

Having no credit history - 56%

Borrowing more than you can afford - 55%

Using too much of your credit limit - 55%

Being registered to vote - 47%

Relationship/Marital status - 23%

Age - 22%

Home address - 22%

Gender - 15%

Checking your score - 12%

If you live with family or friends - 11%

None of the above - 4%

Among the factors we listed, all of them can potentially have some impact on your credit score. However, the degree of impact varies significantly - some factors, like missing credit payments or applying for multiple lines of credit can have a substantial impact, while others, like checking your score or living with family or friends, actually only have a relatively small influence on your credit score.

Tailored financial education for everyone from a young age is crucial for enhancing financial literacy and empowerment. Being aware of your credit score and how to keep it healthy is a cornerstone of financial health, and our analysis highlights the need for continued efforts to ensure that all Brits are equipped with the knowledge they need to make informed financial decisions. Below are some of our top tips for improving your credit score if you’ve found that your credit score is lower than you’d like it to be.

Steps to improve your credit score

If you’re trying to buy a house or a car, or even simply sign up for a mobile phone contract, you’ll be relying on your credit score to get you a good deal. Here are some quick wins and longer-term steps you can take to improve your credit score:

Register to vote

Use less than 30% of the credit available to you on a credit card or overdraft

Check your credit report regularly

Ensure that you pay every credit line on time, every single time

Report any errors on your credit file

Having a bad credit history doesn’t mean that you can’t get the help that you need – when payday is still a way off and you need to cover some unexpected costs like paying for a new boiler or car repairs, you can apply for a loan from Moneyboat might help you out. As a direct lender of bad credit loans, the decision is ours, with no brokers to worry about.

Repaying your loans on time on the agreed dates will benefit your credit score, so if you have a Moneyboat loan, make sure you’re meeting all of your scheduled payments to make sure your credit score doesn’t suffer.

Blog Disclaimer

We do all we can to bring you interesting, practical and valuable information. However, please understand the following:

- Moneyboat.co.uk are in no way connected or affiliated with the application or affiliate links mentioned in this or any article. We do not receive any commission and are not responsible for any charges that may result from any free trials or paid subscriptions.

- Moneyboat.co.uk does not provide medical advice It is intended for informational purposes only. It is not a substitute for professional medical advice, diagnosis or treatment. Never ignore professional medical advice in seeking treatment because of something you have read on the site. If you think you may have a medical emergency, seek medical advice immediately or dial 999.

- Information and data on this blog are for information purposes only. While we work hard to ensure it is accurate, we cannot accept responsibility for the accuracy, completeness, suitability or validity of any information provided on the blog. We will not be liable for any errors, omissions, losses, injuries or damages arising from its display or use. All information is provided with no warranties and confers no rights.

If you feel that any of the information published on our blog is not accurate, please notify us via email at thecrew@moneyboat.co.uk.

Representative Example: Borrow £400 for 4 months: 3 monthly repayments of £156.09 followed by a final repayment of £156.07. Total repayment £624.34. Interest rate p.a. (fixed) 288.35%. Representative 1,267.9% APR.

Compare Moneyboat loans.

Warning: Late repayments can cause you serious money problems. For help, go to www.moneyhelper.org.uk.

Latest blog posts

Celebrating the Easter holidays on a budget

Make sure your Easter celebrations are amazing without breaking the bank. In this guide, see smart shopping hacks, suggestions for dining out for less, and ideas for fun, cheap, local activities over the holidays.

Short-term loans and their advantages

Explore the advantages and disadvantages of personal short-term loans, including payday loans, so you make the right decision when you need funds fast.

How to build an emergency fund

Ready to get started on building an emergency fund? Learn what an emergency fund is, how much to save, and how it can help you avoid short-term borrowing

How to borrow money from family and friends

Learn about family and friend loan agreements and the pros and cons of borrowing money from your loved ones – check to see if it's a good option for you!

What is the difference between APR and interest rate?

Learn the difference between APR and interest rate, how each affects borrowing costs, and why both matter when comparing loans.

Can you pay off a payday loan early?

Wondering if you can pay off a payday loan early? Learn how early repayment works, the pros and considerations, and what to check before you repay.

Why can’t I get a loan?

Wondering why you’ve been refused for a loan? We explore the most common reasons lenders say no, as well as how to increase your chances of approval.

What is a pre-approved loan?

Curious about pre-approved loans and how they work? Find out what loan pre-approval means, whether it guarantees acceptance, and if it’s right for you.