How to Improve Your Credit Rating

For many people, it is a frustrating reality to have been turned down for credit, creating a great deal of stress and concern that you do not have a reasonable chance of being accepted for subsequent loan or credit card applications in the future. One of the most important aspect in these situations is how positive and desirable your credit rating is. Luckily though, there are ways in which to improve your credit score.

However, for some, there may be the requirement of quickly working to boost a credit rating, whereas with others, a slower, more gradual and sustained approach may be what is required.

Understanding your credit rating

It is important to realise and understand that each lender will assess different criteria when deciding to approve or decline your application. This is known as the lenders ‘lending decision process.’

This means that it could very well be the case that you are declined by one company, but accepted for credit by another, as their lending criteria differ slightly from one another. It may be the case that you have to change strategies and apply for credit with a higher-risk lender in order to get access to funds in such circumstances.

Credit Rating and Behaviour

When lenders carry out a credit check, they will be looking at your level of creditworthiness, i.e. how well you have been able to handle any previous debts in the past and the state of your current finances. Whilst this may feel somewhat intrusive, it is all for very good reason.

Such checks are undertaken in order to determine whether or not your past behaviour suggests you will be able to make full repayments if the lender was to approve you for a loan. All that considered though, there are a number of accepted practices to improve your creditworthiness and your desirability to a lender as a prospective borrower.

There are a number of ways in which you can work towards improving your creditworthiness and overall rating.

1. Pay off Outstanding Balances

Always pay off outstanding balances on loans or credit cards before applying for new credit, as this will more than likely be taken into consideration when assessing your application. It is unlikely if you have high levels of existing debt, that you will be accepted for a loan. Alternatively, you may receive higher interest rates if approved, as you will be considered a higher risk due to the outstanding debt(s).

Nevertheless, one should not necessarily assume that having a number of unused credit cards will help you with your score. In fact, such practice may negatively impact your rating, as it does not indicate any aptitude for being able to pay back money promptly. Rather, it would indicate that the prospective borrower has a number of credit facilities available. This may subsequently indicate that the borrower in question lives on credit; beyond their means.

2. Fraudulent Activity

Did you know that it takes the average individual ten months to discover he or she has been a victim of fraud? Check credit card and bank statements every month to identify any unrecognised activity and report it immediately to both your card provider or bank and the government’s fraud department, Action Fraud. The sooner action is taken, the less impact it will have on a person’s credit rating as more can be done to deal with the fraudulent activity, whist the borrower is viewed as responsible and ‘on top’ of their finances.

3. Look for Errors

Mistakes on a credit file are more common than people realise, and they can end up harming your credit rating. However, if spotted they can be easily amended.

It is recommended that you check your credit report at least once a year for this very reason; reviewing your file with each of the main credit reference agencies, as all of them have different information on their files on you. If you see errors, contact the provider in question directly.

4. Build Up a Positive Credit History

Those who have never borrowed money before may be surprised to find they have a hard time gaining access to credit. Lenders regard little credit history in somewhat of a negative light, as they are unable to predict the future behaviour of the borrower. Individuals in this situation should obtain a credit card, use it for small amounts each month and pay the bill in full every month.

5. Request quotes

People often apply for multiple loans or credit cards within a very short period of time to maximise their chance of being accepted for credit by at least one of the lenders. Doing so tends to be a mistake, as each application has the strong potential to lower the person’s credit score. This is why you should request quotes before applying to compare the various financial products. A quote has no impact on a person’s credit rating and will provide the information needed to make an informed decision.

6. Stability is Important

A person who moves from place to place or someone who switches jobs every six months will be a riskier lending prospect than someone who has a stable background and stable circumstances. Instability may indicate that the individual could struggle to make repayments in the future.

7. Register to Vote

One easy way to help improve your credit score is by registering to vote and appearing on the electoral register. This register provides information on who is eligible to vote at an address and it is one of the first things lenders will be checking in order to verify your identity as well as your address history. If you are untraceable, this signals alarm bells for the lender as should you default, you will be harder to contact for repayments.

8. Pay Bills Promptly

Lenders look at the payment history of a person when determining his or her ability to repay the funds being requested. This is why you should make every effort to pay your bills on time to boost your credit rating. Even one missed payment can end up being detrimental to your credit score. If you worry that you may miss a payment, set it up so that the money comes automatically out of your bank account on a regular basis.

Moneyboat's service is rated Excellent

Blog Disclaimer

We do all we can to bring you interesting, practical and valuable information. However, please understand the following:

- Moneyboat.co.uk are in no way connected or affiliated with the application or affiliate links mentioned in this or any article. We do not receive any commission and are not responsible for any charges that may result from any free trials or paid subscriptions.

- Moneyboat.co.uk does not provide medical advice It is intended for informational purposes only. It is not a substitute for professional medical advice, diagnosis or treatment. Never ignore professional medical advice in seeking treatment because of something you have read on the site. If you think you may have a medical emergency, seek medical advice immediately or dial 999.

- Information and data on this blog are for information purposes only. While we work hard to ensure it is accurate, we cannot accept responsibility for the accuracy, completeness, suitability or validity of any information provided on the blog. We will not be liable for any errors, omissions, losses, injuries or damages arising from its display or use. All information is provided with no warranties and confers no rights.

If you feel that any of the information published on our blog is not accurate, please notify us via email at thecrew@moneyboat.co.uk.

Representative Example: Borrow £400 for 4 months, 4 monthly repayments of £149.37. Total repayment £597.48, interest rate p.a. (fixed) 255.5%. Representative APR 939.5%.Compare Moneyboat loans.

Warning: Late repayments can cause you serious money problems. For help, go to www.moneyhelper.org.uk.

Latest blog posts

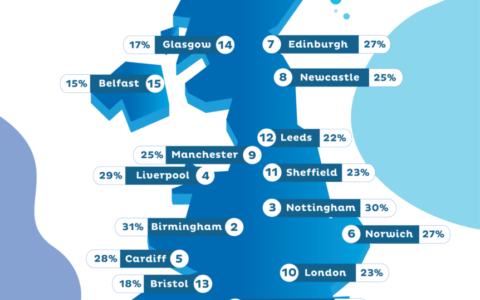

UK Credit Score Index

Curious about UK credit scores and public perceptions? We dive into the world of credit scores and uncover the real emotions and myths around them.